The Total Coverage Blog

Let’s say on one hand you have your home value. On the other, you have the rising cost of building materials. Believe it or not, the two are related courtesy of your homeowners insurance. While this may sound far-fetched, it’s true. Think about this: if something were to happen to your home, what would it cost to rebuild it? And would you be on the hook for some of the bill?

To simplify things, we’re talking about three main players here:

Whether you’re a seasoned homeowner or a first time buyer, it’s important to understand how these three players interact with each other. Let’s start with some new materials.

We’re not here to relive economics class, but supply and demand has played a crucial role in the recent rise in cost of new building materials.

Supply

In the pandemic’s infancy, factories producing materials such as lumber, steel, and cement had to scale back or even shut down manufacturing, thus cutting supply. If that wasn’t enough, materials like paint, plastics, and siding also suffered shortages due to natural disasters, like the big freeze in Texas.

Demand

Meanwhile, the housing market was going wild. Not only were mortgage rates at an all time low, but more people were leaving city life behind to settle down in the ‘burbs (it’s cool to shorten words these days, right?). In other words, more people were willing and able to buy or build homes.

So with demand far outweighing supply, prices have risen. Like, a lot. As reported by the Associated General Contractors of America, between April 2020 and April 2021, lumber alone rose 85.7%.

Now, let’s take a look at how this is related to your home value and homeowners insurance.

About sixty percent of homes are undervalued and potentially underinsured by 17%. This is in part because home projects like renovating your kitchen, finishing your basement, or adding on an addition increase the value of your home.

Now, say something were to destroy your home – a fire for instance. The dwelling coverage part of your homeowners will cover the structure of your home and permanently installed fixtures (think wiring and plumbing). With the high cost of building materials, you may find yourself underinsured.

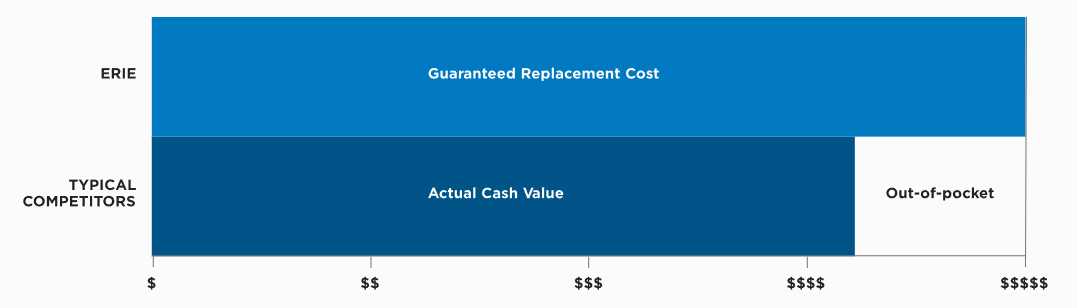

It’s also important to think about what your policy will actually cover. There is a big difference between actual cash value vs. replacement cost. With actual cash value, you may have lower premiums, but your loss will be restored minus depreciation. Whereas with replacement cost (like Erie’s Guaranteed Replacement Cost), your rebuilt home will be equivalent to what was lost.

We recommend checking in on your homeowners insurance policy each year or after any major home projects. While reassessing your home value will inevitably raise your premiums, you will be able to rest easy knowing that you’re covered if something were to happen to your home. Plus, by speaking with your local agent, they may be able to find ways to help offset the increase!

Need a home quote? Curious about Guaranteed Replacement Cost? See what we can do for you.

Let’s Get Started

Downtown Denver

Unruh Insurance Agency, Inc.

335 Main Street

Denver, PA 17517

P: 717-335-2929 | F: 717-335-2923

Shady Maple Complex